U.S. Stocks Move Sharply Higher Amid Optimism The Fed Is Done Raising Rates

After moving mostly higher early in the session, stocks saw further upside over the course of the trading day on Wednesday. The Dow closed higher for the third consecutive session, climbing further off last Friday’s seven-month closing low.

The major averages pulled back off their highs going into the close but held on to strong gains. The Nasdaq surged 210.23 points or 1.6 percent to 13,061.47, the S&P 500 jumped 44.06 points or 1.1 percent to 4,237.86 and the Dow advanced 221.71 points or 0.7 percent to 33,274.58.

Stocks saw continued strength later in the session amid a positive reaction to the Federal Reserve’s widely expected decision to leave interest rates unchanged.

The Fed said it decided to maintain the target range for the federal funds rate at 5.25 to 5.50 percent, marking the third time in four meetings that the central bank has refrained from raising rates.

The accompanying statement suggested the Fed is still considering additional rate hikes in an effort to return inflation to its 2 percent objective, but traders seem optimistic the recent cycle of increase is over.

“The Fed tried to deliver a hawkish hold but Wall Street is not believing additional tightening will happen this cycle,” said Edward Moya, senior market analyst at OANDA.

The latest statement also said, “Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation.”

The Fed’s September statement only cited “tighter credit conditions,” with the inclusion of “financial” coming amid the recent surge in treasury yields.

“Some might take this as a sign that the bond market will continue to help them with this tightening cycle, which could support the argument that a peak in rates is in place,” said Moya.

The early strength on Wall Street came as the release of some weaker than expected U.S. economic data eased concerns about the outlook for interest rates.

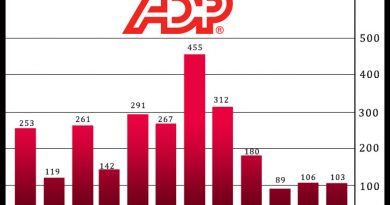

Payroll processor ADP released a report before the start of trading showing private sector employment in the U.S. increased by less than expected in the month of October.

The report said private sector employment climbed by 113,000 jobs in October after rising by 89,000 jobs in September. Economists had expected employment to jump by 150,000 jobs.

A separate report released by the Institute for Supply Management showed manufacturing activity in the U.S. unexpectedly contracted at a faster rate in the month of October.

The ISM said its manufacturing PMI fell to 46.7 in October from 49.0 in September, with a reading below 50 indicating a contraction. Economists had expected the index to come in unchanged compared to the previous month.

Sector News

Housing stocks moved sharply higher over the course of the session, resulting in a 3.5 percent spike by the Philadelphia Semiconductor Index.

Substantial strength was also visible among semiconductor stocks, with the Philadelphia Semiconductor Index surging by 2.3 percent. The index climbed further off the five-month closing low set on Monday.

Advanced Micro Devices (AMD) led the way higher after reporting better than expected third quarter earnings and providing upbeat guidance for its AI chip business.

Computer hardware stocks also saw considerable strength on the day, as reflected by the 1.9 percent jump by the NYSE Arca Computer Hardware Index.

Software, retail and biotechnology stocks also showed strong moves to the upside, while networking, telecom and tobacco stocks bucked the uptrend.

Other Markets

In overseas trading, stock markets across the Asia-Pacific region moved mostly higher during trading on Wednesday. Japan’s Nikkei 225 Index surged by 2.4 percent, while South Korea’s Kospi jumped by 1.0 percent.

The major European markets also moved to the upside on the day. While the U.K.’s FTSE 100 Index rose by 0.3 percent, the French CAC 40 Index and the German DAX Index advanced by 0.7 percent and 0.8 percent, respectively.

In the bond market, treasuries moved notably higher early in the session and remained firmly positive throughout the day. Subsequently, the yield on the benchmark ten-year note, which moves opposite of its price, slid 8.6 basis points to 4.789.

Looking Ahead

Trading on Thursday may continue to be impacted by reaction to the Fed announcement, while reports on initial jobless claims, labor productivity and factory orders may also attract attention.

Source: Read Full Article